**Mike Roberts**, Principal Consultant - Service Provider

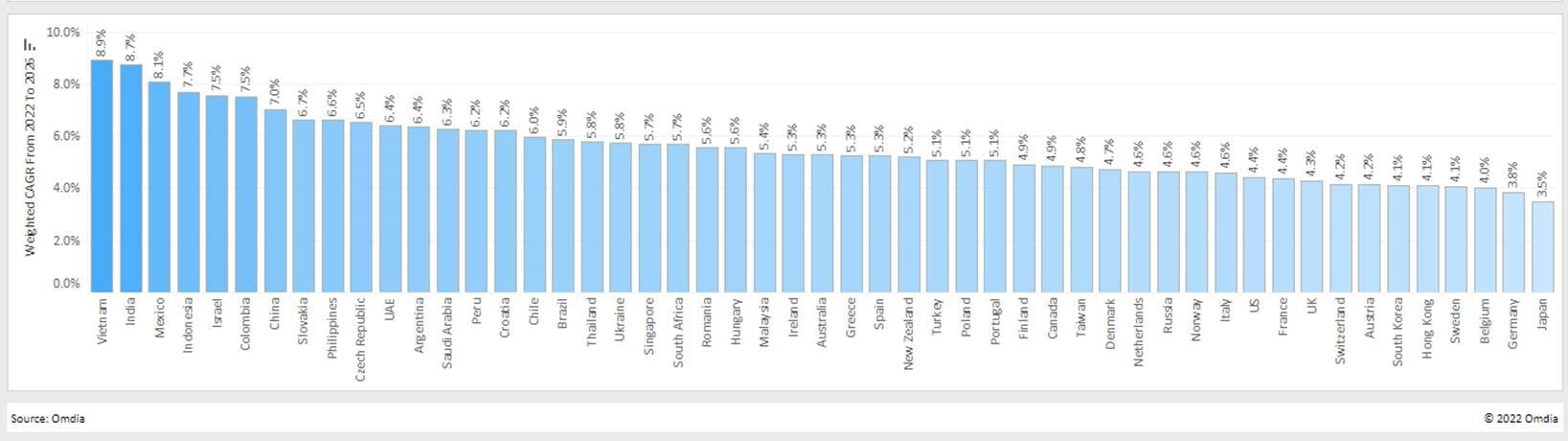

Vietnam will have the strongest digital growth over the forecast period of all the 51 countries in the Index, with a weighted CAGR of 8.9% from 2022 to 2026.

India will not only record the second-fastest digital growth of 8.7% from 2022-26 but will also maintain its position as the third-largest digital economy over the period, behind only China and the US.

Mexico will record the third-highest digital growth of countries in the Index, with a weighted CAGR of 8.1% from 2022 to 2026. It will maintain its position as the thirteenth largest digital economy throughout the period.

Indonesia will see a digital growth of 7.7% from 2022-26, the fourth-highest in the Index. That strong growth will lead Indonesia pass South Korea in 2025 to become the ninth-largest digital economy in the Index.

Aligning government policy and private investment to spur digital growth

Extending digital infrastructure and services to underserved communities

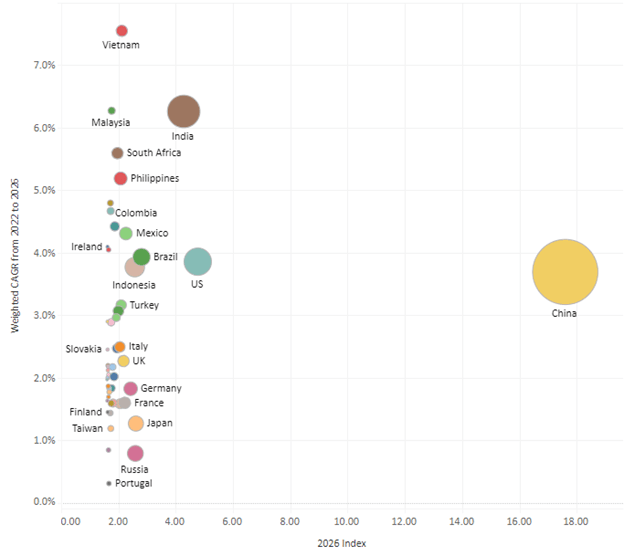

FT Omdia Digital Economies Index – Connectivity Growth

4. India's telcos weather pandemic - In 2021, India’s economy showed signs of a post-pandemic revival, on the back of easing government restrictions and shops reopening. The telco sector, the key provider of digital connectivity, remained largely resilient in the face of COVID-19.

5. Mexico strong in Enterprise IT - The enterprise IT market in Mexico will grow 12.4% from 2022-26, the third-highest rate in the index, spurred by a 17.2% growth in cloud spend over the period. Mexico will also see robust growth of 7.8% through 2026 in devices & IoT.

6. Indonesia returns to growth - Omdia is forecasting that Indonesia’s digital markets will see strong growth through 2026, following recent signs of broader economic recovery including the 5.01% year-over-year (YoY) growth of Indonesia’s GDP in 1Q22 compared to 1Q21.

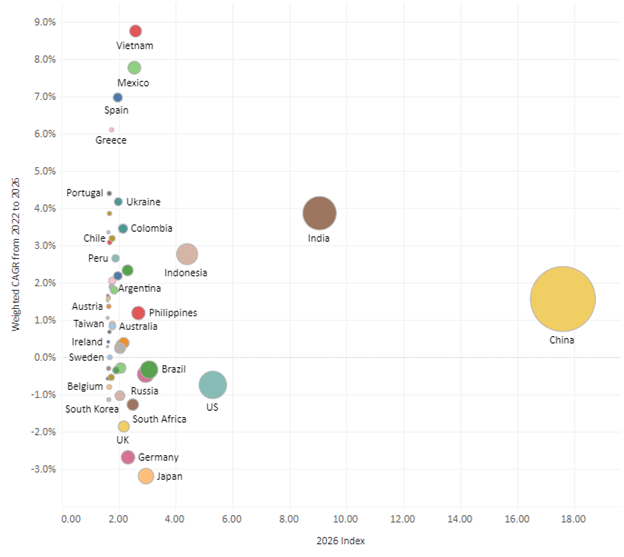

FT Omdia Digital Economies Index – Devices & IoT Growth

The Vietnamese government has stated its ambition to achieve 100% smartphone penetration by 2023, which will significantly accelerate both digital connectivity and the use of digital services. Furthermore, e-commerce has been significantly gaining traction across the country, including in rural areas, accelerating the trend. Local telecommunication operators Viettel and VNPT have also launched digital financial services (mobile money) to complement its telecommunications business and various other businesses.

Vietnam is also one of the key markets for foreign direct investment in South-Eastern Asia, especially for the manufacturing industry. This will help to increase digital investment and growth in one of the largest industries in the country.

Launching in India in 2022, 5G will account for more than 20% of mobile subscriptions in the country within three years; 4G took five years to reach that level of penetration. Omdia is currently forecasting that there will be 370 million 5G subscriptions in India by the end of 2026, representing close to 30% of the mobile market.

In the consumer segment, 5G adoption in India will benefit from the fact that an increasing number of mobile subscribers have smartphones that support 5G, even before 5G commercial services and network coverage have launched in the country.

In addition, Omdia recently conducted a survey of 316 enterprises in India that shows companies are ready to adopt 5G services, with 52% saying they want to start using 5G services in 2022 or 2023 and another 31% expecting to use 5G in 2024.

In Mexico, as in many emerging markets, Omdia believes that more regulatory and public policy initiatives are required to expand telecoms network coverage, which would in turn reduce the digital divide in the country.

The country’s telecoms regulator – the Federal Telecommunications Institute – has issued a new set of guidelines for the deployment, access, and shared use of telecom and broadcasting infrastructure that would go a long way toward reducing the rural–urban disparity in the country.

However, the government should also ensure sufficient fund allocation to the sector through its annual budgets as there is a lack of proper connectivity in the remote and rural parts of the country.

In 2022, despite major global crises, such as the Russia-Ukraine war, rising inflation rates, and supply disruptions, Indonesia’s telecoms market remained robust, leading Omdia to maintain its forecast for growth in the country’s mobile and fixed broadband markets.

Also in 2022, all operators in Indonesia announced their plan to accelerate the migration of 3G users to 4G, and to upgrade their network assets to cope with the increased demand for data. This will lead to increased data consumption and data service revenue over time. Indonesia is seeing ongoing growing demand for fixed broadband services, with service providers continuing to expand their fiber footprint.

Omdia recently conducted a survey of 316 enterprises in India that shows companies are ready to adopt 5G services, with 52% saying they want to start using 5G services in 2022 or 2023 and another 31% expecting to use 5G in 2024.

FT-Omdia Digital Economies Index - Country by Total Growth, 2022 - 2026

Mike Roberts Principal Consultant, Service Provider mike.roberts@omdia.com