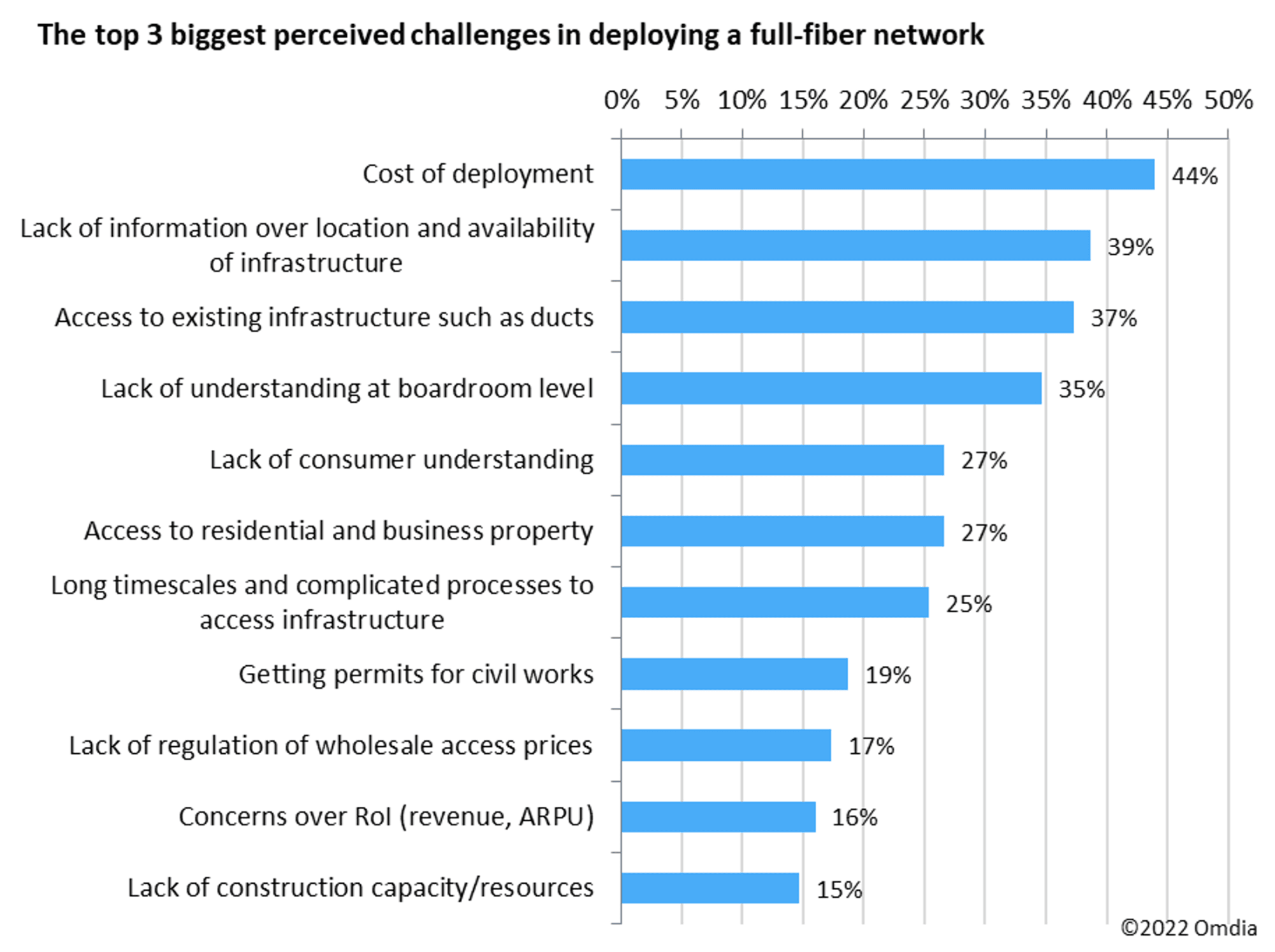

Operators looking to deploy fiber infrastructure face many challenges, some of which require intervention from regulators and governments to overcome them. In a survey by the World Broadband Association of 75 broadband operator senior executives, cost of deployment—as perhaps to be expected—was highlighted as the number one perceived challenge, closely followed by a lack of information on the location and availability of key infrastructure, as well as easy access to that infrastructure (see Figure 15).

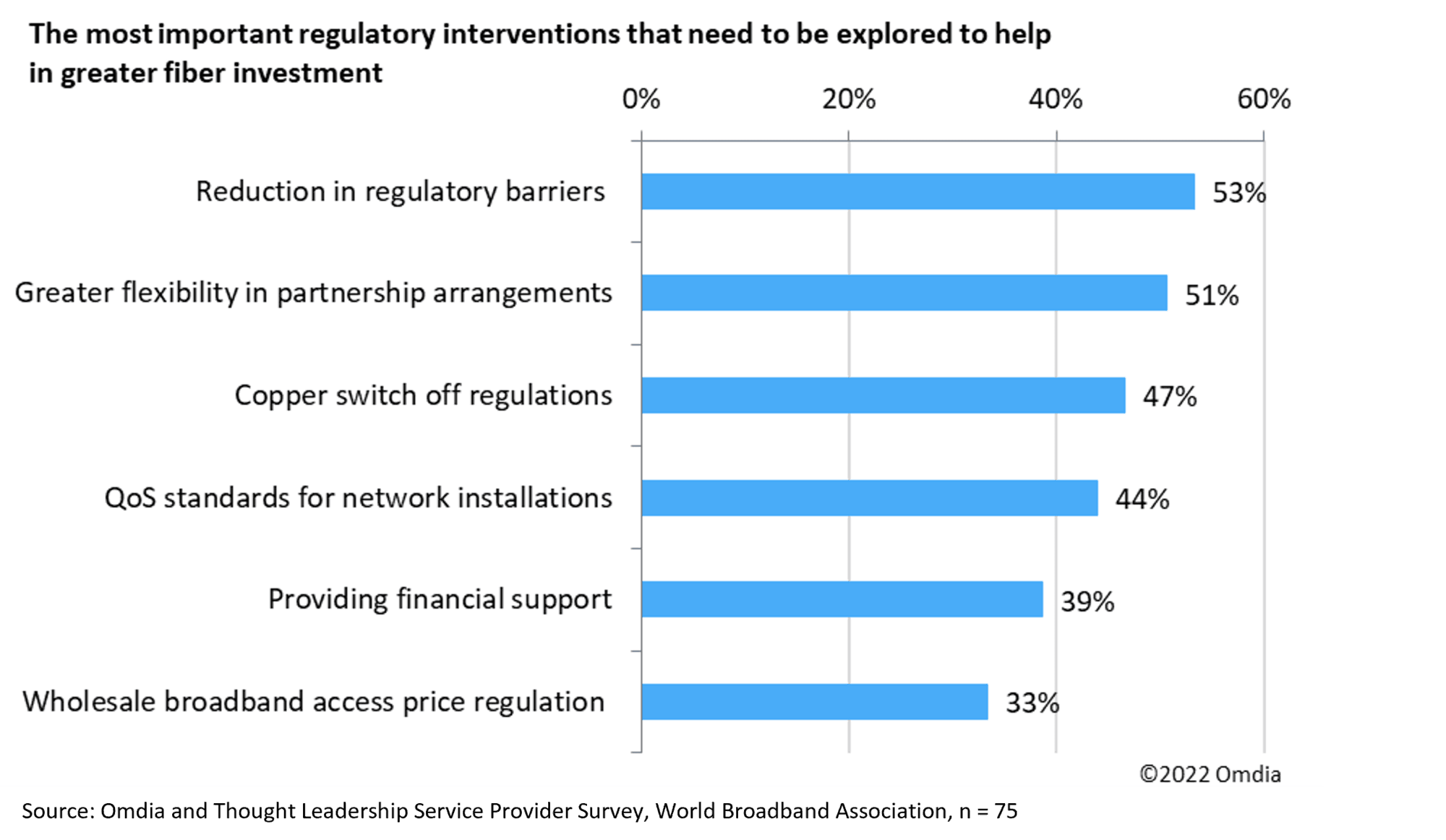

When asked about areas where governments/regulators could help, the survey found that it is less about financial assistance (although that will still be necessary in most territories to connect the really hard-to-reach customers) and more about providing greater flexibility and changing regulations where possible to make fiber investment easier (see Figure 16). Legislation to make it easier to locate and gain access to key infrastructure such as ducts, poles, and so on would also help with new infrastructure deployment. More complex legislation should also consider non-telecom infrastructure, such as access to infrastructure deployed for other utility purposes, to gain maximum efficiencies.

Therefore, regulation and public policy have a key role to play in removing any barriers, and a better-connected world can only emerge if there is collaboration between governments, regulators, and operators to encourage investment. While governments and regulators can set clear connectivity targets and lower the financial and regulatory barriers to broadband access, private investment must also be fostered and conditions for good levels of competition must be set.

Figure 15 : Cost of deployment is not the only hurdle when deploying full-fiber networks

Figure 16 : Financial support is not the only help governments can provide

There are several regulatory policies that are seen as best practice for encouraging the deployment of very high-capacity networks, such as:

The pandemic has highlighted the remaining holes in broadband maps and reinforced the need to close the digital divide and designate networks as critical infrastructure. So, ubiquitous broadband access is a key element in any country’s digital agenda. High-speed network rollout is often commercially viable only in densely populated areas; therefore, nationwide deployment will normally require some form of government funding. The key challenge is ensuring widespread broadband rollout is funded while also being fiscally sustainable and still preserving private incentives to invest. This challenge will grow in the coming years when economically viable areas are covered, but the gap in rural regions with scattered populations widens.

Various forms of financing are being used to ensure that these areas are not left behind—for example, publicly built networks (e.g., Australia and Argentina); publicly built municipal networks (e.g., Sweden and Germany); public-private partnerships (PPPs) (e.g., Mexico and Peru); direct/indirect subsidies (e.g., the EU); physical resources access, that is ducts, poles, and land access (e.g., Mexico and Sweden); and regulatory coverage or service obligations (e.g., Chile and Brazil). There is no single right answer, but at the very least, governments should get more involved in guaranteeing broadband connectivity for all citizens. However, it is also crucial to adopt the most suitable investment model to reflect national circumstances. This doesn’t necessarily involve a state-owned company that is controlled and financed by the government—public-private partnerships or private-led deployment with government incentives could be more relevant in some cases. Regardless of the model, best practice dictates that any state intervention must limit the risk of crowding out or replacing private investments, altering commercial investment incentives, or distorting competition.

To varying degrees of detail, most countries around the world have outlined some form of national broadband plan. For the less economically developed nations, these plans should focus on improving broadband coverage before looking to expand high-speed networks such as fiber. Meanwhile, the more progressive countries should focus on developing national digital strategies. Developing comprehensive national digital strategies that ensure citizens can use connectivity in a transformative way to bring about innovation and growth, rather than focusing purely on broadband infrastructure deployment, will be crucial in building the case for fiber deployment and encouraging further investment.

National broadband plans aim to only guarantee infrastructure availability and deployment and have proven insufficient on their own since the targets of many countries have not been achieved, so gaps are widening. Governments that have seen the most success have been those that proactively prioritize developing their own unique, integrated, and comprehensive national digital strategy for both broadband infrastructure and how to get citizens to use it effectively. Combining these strategies to reflect each country’s resources and capabilities maximizes the benefits of digital transformation for innovation, growth, and social prosperity. Within the best digital strategies, governments still tend to set coverage objectives in an effort to ensure that connectivity continues to improve on an ongoing basis. Leaders agree that unlocking the benefits of ongoing digital transformation means addressing the challenges this creates, particularly for jobs, skills, and trust. A few advanced countries have already defined their national digital strategy, but many more are expected to do so in the coming years.

There are many examples of governments around the world that have already moved from pure national broadband infrastructure deployment plans to comprehensive national digital strategies. The UK, for example, launched its national digital strategy in 2017. The strategy looks at connectivity, digital skills and inclusion, development of digital sectors, helping businesses go digital, cybersecurity, digital government, and unlocking the power of data. Meanwhile, Singapore’s Infocomm Media 2025 plan has three main pillars: capitalize on big data and analytics, deepen the converged industry ecosystem, and better connect people. The first phase, involving extending connectivity through the deployment of above-ground boxes and technologies from a heterogeneous network (HetNet), was completed at the end of 2015. The other two phases involve introducing real-time data collected through a mesh of sensors nationwide.

In addition to introducing a national broadband plan and digital strategy, many regulators look to implement a universal service obligation (USO) to ensure that basic telecoms services are available at an affordable price to all households and businesses. For many countries, functional internet access has been included in universal service obligations for some time. However, this has usually been defined as basic dial-up speeds. But as demand for greater data volumes increases and with improvements in average connection speeds, there is an argument for introducing a broadband USO that better reflects today’s technological capabilities. However, these are mostly in mature markets, and usually the broadband speed targets that have been adopted are fairly low, ranging from 1Mbps to a potential 30Mbps. Smaller countries are generally ahead on this issue, but larger countries are catching up. Most of the countries where broadband USOs have been introduced are geographically relatively small. That is hardly surprising since small countries are more easily covered in a ubiquitous way—for example, Singapore, where an operator faces a USO to install fiber-optic connections upon request. It is clear that regulators and policymakers cannot rely on market forces alone to deliver ubiquitous high-speed broadband without some kind of regulatory intervention, but universal service obligations have not been universally proven to be the best means of achieving this goal. Rather than explicitly setting universal service obligations to install fiber connections, many countries have instead been using the universal service funds as a source of financing to support one-off investment projects to deploy higher capacity networks.

As legacy copper networks become harder to maintain, operators around the world are starting to consider phasing them out, but this generally requires input from regulators. It is important to retire legacy copper networks so that incumbents do not encounter the unnecessary costs of running two parallel networks and can free up investment for further fiber deployment. Best practice for countries heavily reliant on copper commands that migration away from copper does not cause disruption for consumers. Therefore, some regulators have imposed minimum notice periods to minimize the effect on the market and ensure the transition is carried out under fair and competitive terms. This needs to be coupled with the removal of regulation on the incumbent’s copper products in areas where full fiber is built and the transfer of regulations, including price protections, from copper to new fiber services during the transition. This would encourage customers to switch over to the new fiber network, while also protecting them during the transition period and thereby building the case for more investment in underserved areas. Until the deployment of fiber has been sufficiently accelerated, it is better for regulators to continue not to regulate full-fiber services. In Spain, for example, fiber services offering speeds of more than 30Mbps have not been regulated, and full-fiber investment has been successfully stimulated, with fiber cables being rolled out not only by the incumbent but also by its rivals.

Facilities sharing is becoming an increasing focus for regulators as the desire for competition in next-generation network deployments grows. In markets where there is the perception of market failure, through lack of attainment of national broadband plan objectives, regulatory intervention in infrastructure sharing can be beneficial. To encourage private investment in fiber infrastructure, barriers to entry and the cost of laying fiber need to be addressed, access to ducts and poles must be simplified, and a stable regulatory environment needs to be maintained. Comprehensive passive infrastructure regulation has had a significant impact on the deployment of next-generation networks.

Alternative operators generally attribute high importance to the presence of offers of passive infrastructure access. Regulatory approaches do vary, though. Those that have seen the greatest success rely on a clear, simple, and certain regulatory framework and on an effective dispute-resolution process, as well as on outlined maximum timelines regarding repairs and installations. Transparency can be assured with the use of online broadband network maps. It is good practice that the role facilities sharing takes in a given country varies according to the degree that competitive outcomes are supported by infrastructure-based competition and the level of intervention perceived to be necessary to achieve investment. Best practice often involves regulators adopting a combination of symmetric and asymmetric regulation. Symmetric regulation has been extended in some markets to include utilities and asset owners beyond the communications industry because there is increasing recognition of the need for investment coordination within the sector and with other infrastructure verticals. Meanwhile, asymmetric regulation remains a key tool for regulators in recognition of the ownership of bottleneck assets by incumbent service providers. Spain is a market with considerable asymmetric regulation, as Telefónica alone is subject to duct and pole access (DPA) obligations. DPA regulation can also be limited to certain use cases (e.g., allowing access to ducts to support fiber-to-the-x [FTTx] deployments).

The early adoption of a facilities-sharing policy contributes to improved fiber connectivity availability. In countries with significant uptake of duct access, this has driven infrastructure-based competition in next-generation access (NGA) broadband. Requiring incumbents to grant access to telegraph poles and underground tunnels to all alternative providers makes it quicker and easier for them to build their own full-fiber networks, which cuts the upfront costs associated with laying fiber cables by approximately 50%, a considerable incentive for investment.

Access to other civil engineering and rights of way are also vital to rolling out fiber networks. Ensuring a streamlined approach to permit-granting procedures for civil works is essential, and the best way of achieving this is to adopt a single information point where operators can access information and apply for permits for civil works.

The final few meters of a wired-broadband network can often be the most complex part because, more often than not, it will cross privately owned land or some type of building such as an apartment block (often referred to as a multi-dwelling unit or MDU). It is one of the advantages of wireless broadband technologies that they can bypass this requirement and, therefore, greatly speed up installation.

However, for wired-broadband operators to gain access to the building or to cross private land, they must have a written agreement (known as a wayleave agreement) from the land or property owner, which, due to simple logistics, can cause a significant bottleneck to deployment. If not regulated properly, in-building access agreements in the case of large MDUs can also lead to a form of service monopoly where residents of that MDU can only access a certain service provider as only that service provider has access to the building.

To stimulate greater FTTH deployments, therefore, it is vital that national regulations are created that simplify the wayleave-agreement process and that wholesale agreements are put in place that provide fair access for all operators looking to access that building.

To accelerate future rollouts, property developers could help by preinstalling fiber infrastructure in the buildings and local areas. Preinstallation of fiber-optic cables reduces cost and disruption caused by any future deployments. Therefore, governments should explore schemes that guarantee such investment as part of the planning process. In France, for example, a preinstallation policy was put in place back in 2008 as part of its “Law for the Modernization of the Economy” scheme, which required all new residential developments to be equipped with optical fiber. China has also since adopted a similar policy. In other countries, such as New Zealand and Singapore, property developers are not mandated to preinstall fiber, but they can opt to be connected to the fiber network, making the development more attractive and saving future costs and disruption.