One of the most cited barriers in fiber rollouts is either the lack or inefficiency of regulation. To promote fiber development, governments must adopt concrete legislation that targets inefficiencies such as insufficient access to existing telecoms and public infrastructures, improves rights of way, and promotes investment and partnership agreements

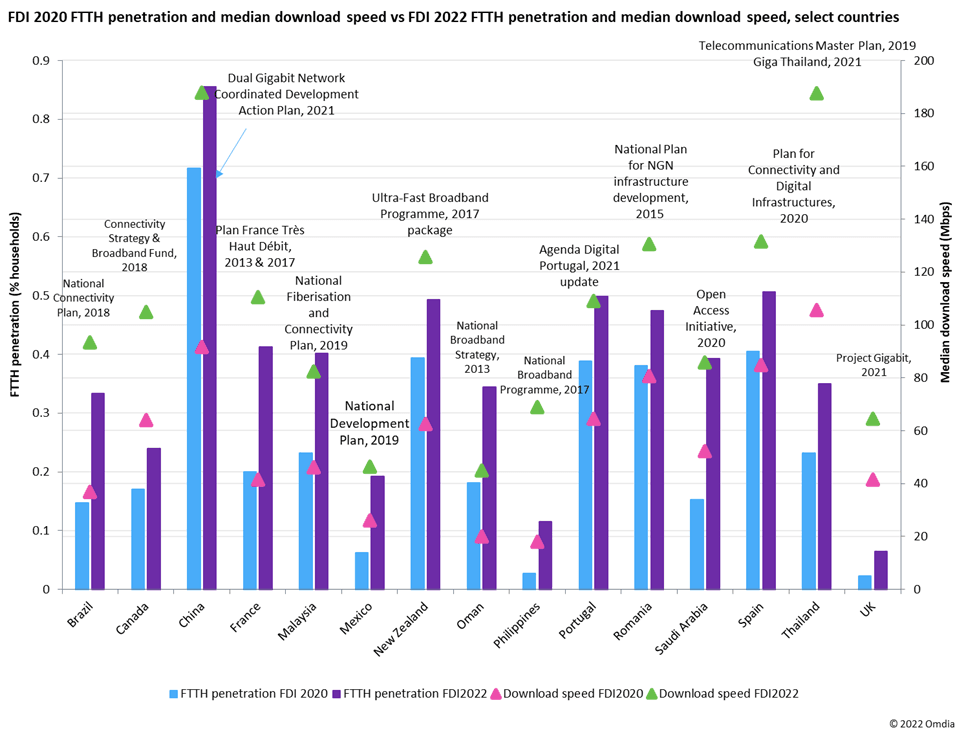

Most countries in the FDI have a national broadband agenda in place; however, it is not enough to publish a national broadband strategy without also ensuring its implementation. Successful countries follow through on their broadband initiatives, creating sufficient supporting funding and tracking progress of reaching the goals set out in the broadband plans, while taking advantage of new technologies and innovations that may be better suited to achieve these targets. Generally, there tends to be a significant lag between a national broadband strategy’s introduction and the tangible results being noticeable in the field. However, a review of select markets that have seen significant improvements in fiber uptake, median download speeds, and regulatory policies implemented over the last couple of years clearly shows a positive impact on fiber development in these countries (see Figure 14).

Some countries, such as France or the UK, have only recently recognized the importance of fiber in their national broadband strategy and have since made significant and rapid progress in fiber deployment. In 2021, the UK government launched a £5bn government infrastructure project called “Project Gigabit,” aimed at getting gigabit broadband access to more than one million hard-to-reach homes and businesses. In France, the 2017 amendment to the original 2013 ultra-fast broadband plan (Plan Très Haut Débit) gave preference to fiber over other access technologies. In Brazil, a 2017 revamped version of the national broadband plan originally drafted in 2010 also seeks to expand fiber-based network throughout the country. The strategy passed a bill modifying the country’s telecom legislation, unfroze resources from the telecom universalization fund, and modified fines-for-investments deals between telecom regulator Anatel and telecom operators. The approach has led to substantial improvements in both fiber access and quality of experience for consumers.

In other countries, additional funding and amendments to existing strategies were necessary to boost broadband network deployments in hard-to-reach areas. In New Zealand and Canada, funding packages adopted in 2017 and 2018, respectively, have led to fiber-network expansions. In Oman, there was a delay between strategy adoption and securing sufficient funding. Oman’s government adopted its National Broadband Strategy in 2013 but did not receive financing for its fiber network rollout from the Asian Infrastructure Investment Bank (AIIB) until 2017. A second financing extension from the AIIB was awarded in 2021. Only after the government was able to secure this investment has the country seen a substantial increase in fiber deployment and uptake.

Focusing on cooperation among network operators is an essential part of successful gigabit broadband strategy, as recognized by the Saudi Open Access Initiative adopted in 2020. All six telecommunications companies entered into the Open Access agreement, guaranteeing the provision of broadband services through any subscriber-selected service provider, independent of infrastructure ownership.

Figure 14 : National broadband plans and initiatives and progress in FDI metrics for select countries

China continues to be one of the most ambitious countries when it comes to connectivity targets, especially considering the size of the country and scale of the population. The country now sits in third position in the Fiber Development Index, having witnessed the highest increase in its FDI score out of the top 10 countries.

The State Council launched its national broadband strategy—Broadband China—in 2013. Initially the increasing ratio of FTTH users was slow. In 2014, to push forward with the fiber access network construction, the MIIT together with the MHURD made a joint announcement about the new national standards for fiber preinstallation and sharing with operators in new buildings. The strategy created a clear requirement for fiber cabling and installation engineering and removed obstacles from property management organizations. According to the new standards, before new buildings receive a sales permit, the access fibers to every household and the rooms for communication device deployment must be completed and have passed the acceptance tests. All engineering costs should be covered by building developers. With the strong support from the government, the fiber access ratio among all broadband users increased significantly from 2015. By the end of 2021, 99% of homes in China had access to FTTH technology, and FTTH penetration sat at 85%.

Between 2016 and 2018, the MIIT and the National Development and Reform Commission (NDRC) led a three-year action plan for the construction of communications infrastructure, with a budget of CNY1,200bn ($181bn). The plan aimed to support the development of high-speed fiber optics, the construction of advanced mobile broadband systems, and global network facilities. To execute this plan, the government focused on 92 selected infrastructure projects, with a total investment budget of CNY902.2bn ($136.3bn). Prioritizing certain projects allowed the government to focus on the areas most in need.

In 2019, the MIIT then proposed a “dual-gigabit acceleration, same speed for same network” plan to promote fixed-broadband gigabit applications in order to keep pace with bandwidth-hungry services. This involves utilizing 10G Passive Optical Network (PON) technology to create a dual gigabit broadband service that features both wired and wireless gigabit broadband.

There is currently no regulation imposing a broadband USO across the entire country. However, the MIIT supports the upgrade of fiber broadband in 130,000 administrative villages, including 43,000 poor villages. By November 2018, 96% of administrative villages achieved optical-fiber access, and the country expanded broadband infrastructure to 94% of underserved villages. This was ahead of schedule according to the country’s broadband strategy, which required operators to expand broadband infrastructure to 98% of underserved villages by 2020.

In 2021, China shifted its focus from broadening the coverage of the fiber network to increasing the speed and improving the quality of broadband services. In March 2021, the MIIT released a plan to expand the gigabit network to cover 200 million people by the end of the year and 400 million by the end of 2023. The government targeted 10 million gigabit users by the end of 2021—a goal it smashed, with more than 34 million 1Gbps users at the end of 2021 and just under 46 million by March 2022. As of the same date, 93% of broadband users had access to speeds of 100Mbps, and as of June 2022, China had the third-fastest median broadband speed in the FDI.

The European Union, through its European Commission (EC) governing body, sets out policies to encourage digital opportunities and enhance Europe’s leading position in the digital economy. In May 2015, the Digital Single Market (DSM) strategy was adopted to eliminate online barriers. These barriers hamper free movement of goods and services online and mean that businesses, governments, and individuals cannot fully benefit from digital tools that would be available to them but that are currently locked in 27 different regulatory environments.

The EC estimates that once completed, the DSM could create up to €415bn per year and generate hundreds of thousands of new jobs. The DSM strategy is based on three pillars:

However, for consumers, businesses, and governments to fully benefit from the provisions of the DSM, it is essential that access to digital infrastructure is ensured by facilitating rollout of reliable, high-speed broadband networks across Europe. In September 2016, the EC introduced a new set of competitive Gigabit Society connectivity targets to be achieved by 2025. These targets include:

• All main socioeconomic drivers, such as schools, transport hubs, and main public service providers, as well as digitally intensive enterprises will have gigabit connectivity.

Moreover, the Digital Compass communication adopted in March 2021 set out ambitious “Digital Decade” 2030 targets, which further highlight gigabit connectivity for everyone and 5G coverage everywhere by 2030. In September 2021, the “Path to the Digital Decade” proposal then identified and confirmed the importance of investment-friendly regulatory and policy frameworks, which would facilitate collaboration between national and EU-level policies and foster investment to achieve the Digital Decade 2030 targets. This framework includes stipulations for multi-country projects under the auspices of the newly established European Digital Infrastructure Consortium (EDIC). Under the EDIC procedure, at least three member states can present large-scale projects that facilitate the digital transformation targets and channel coordinated investments between the EU, the participating member states and, where applicable, other public or private stakeholders.

In addition to its digital strategies, the EC also sets forth concrete policies focused on broadband infrastructure deployment. In 2014, the EU established the “Broadband Cost Reduction Directive,” which aimed to “facilitate and incentivize the rollout of high-speed electronic communication networks.” The regulation promoted measures for facilitating the joint use of existing physical infrastructure and more efficient deployment of new physical infrastructure at a lower cost. The EU member states implemented the directive into their national rules. However, in 2018, the EC reviewed the directive’s implementation and found problems related to its efficiency and consistency.

In 2020, the EC launched a further review and created the European Electronic Communications Code to improve the regulatory conditions to incentivize private investment and deploy and take up high-speed broadband networks. The European Electronic Communications Code also addressed the timely and investment-friendly access to the 5G spectrum. The EU instructed member states to transpose and apply the code’s provision by December 21, 2020.

In September 2020, the EC adopted a recommendation calling for all member states to develop and agree on a common Union toolbox of best practices to foster connectivity. In terms of reducing network deployment costs, the best practices are as follows:

As a result of the unified digital strategies and regulations, there has been great improvement in fiber availability and take-up across the EU, with Romania and Spain ranked in the top 10 countries/territories in Omdia’s FDI and Denmark, Sweden, and Portugal in the top 15. However, there remain large differences among the EU member states in terms of fiber rollout, and penetration and achieving universal gigabit connectivity will be challenging in some markets.

With 32% of the country’s population still accessing the internet only through mobile networks and with just 56% fixed-broadband household penetration, Thailand could still be thought of as a largely “mobile-first” country. However, 63% of those connected households are connected via FTTH technology, and so where broadband is available, the QoE is very high. Therefore, Thailand already sits in seventh place in the Fiber Development Index. The challenge for the Thai government now, therefore, is to continue to expand the fiber coverage and encourage further take-up.

The aim of the original Thai national broadband plan was to cover 95% of the population with its fixed-broadband network by 2020, but it missed this target by some margin. Where the country has been successful is in its fiber-first broadband strategy, achieving FTTP coverage of 56% at the end of 2021.

Fiber is seen by the Thai government as a key investment to drive economic growth and to make Thailand an “ASEAN digital hub.” In November 2021, NBTC announced a partnership with Huawei at an event—Giga Thailand: Broadband Forum—to accelerate fixed-broadband coverage and upgrade to gigabit-speed standards.

Under new policies set out by the Thailand Digital Economy and Society Development Plan from MDES (MDES Action Plan 2018–22, and ONDE Action Plan 2022–27), the Thai government developed five key targets related to the development of fixed-broadband networks:

In 2018, the Malaysian Communications and Multimedia Commission (MCMC) carried out a review of its national broadband strategy and found a number of performance challenges that were holding back the country’s broadband development. Although at that time broadband services were available to 92% of the population in populated areas, rural areas were still less well served. It also found that even where available, the quality of the broadband infrastructure could also be low, while prices were still relatively high.

The organization, therefore, set out its “National Fiberisation and Connectivity Plan (NFCP) 2019-2023,” with the specific aim of

To meet these aims, the MCMC set out a new fiber-first national broadband plan with the following targets:

The results of these initiatives are that FTTP coverage is now 53% (up from 45% in 2020) and FTTH penetration is 40%. Overall broadband speeds, however, are still quite low, and the government should look to policies that will encourage greater investment in the fiber core to enable more advanced broadband services and applications in the future.