John Kendall - Principal Analyst Taimur Zafar - Research Analyst

Consumer expectations of their home networks have rapidly evolved in recent years. Work, study, and entertainment are all expected at ever-increasing levels from home networks, with concurrent usage adding significant strain. This increased expectation must be met, either through the service provider or retail channel. This will intensify the battle between service providers and large technology companies for control of the home network. Technological advantages will be key to differentiating offerings.

Wi-Fi 6E will be a key development for home networks, with access to the 6GHz band opening a large amount of spectrum for Wi-Fi traffic, reducing congestion in the home. The key benefits of the new Wi-Fi 6E standard will be faster connectivity, reduced latency, and less spectrum congestion. The major negative is that shorter wavelengths reduce penetration, meaning Wi-Fi range is negatively affected particularly in homes with thick walls. Retail vendors are the first to offer this technology. Service provider vendors could focus on Wi-Fi 6E hardware at MWC to allow service providers to remain competitive with retail offerings.

Whole home Wi-Fi systems will be another key area for home networks, with a multitude of retail options available at a range of price points. At MWC, service provider CPE vendors could show some developments with their whole home Wi-Fi systems. Retail vendors have dominated this area, with whole home Wi-Fi being primarily an innovation of the retail channel. Whole home systems require access points throughout the homes of consumers, and this type of set up solves the penetrations problem presented by the shorter wavelength Wi-Fi 6E.

At MWC, CPE vendors should help service providers reduce the technological advantage that retail vendors have built by offering Wi-Fi 6, whole home Wi-Fi, and additional services for the home network. Retail vendors will, in turn, need to differentiate their offerings to attract customers from service providers by using the home network as a platform for other services. Deeper smart home support, access point integration into other devices, and additional services will be key methods for differentiation. With both large technology companies and service providers vying for control of the home network, exciting innovation is guaranteed.

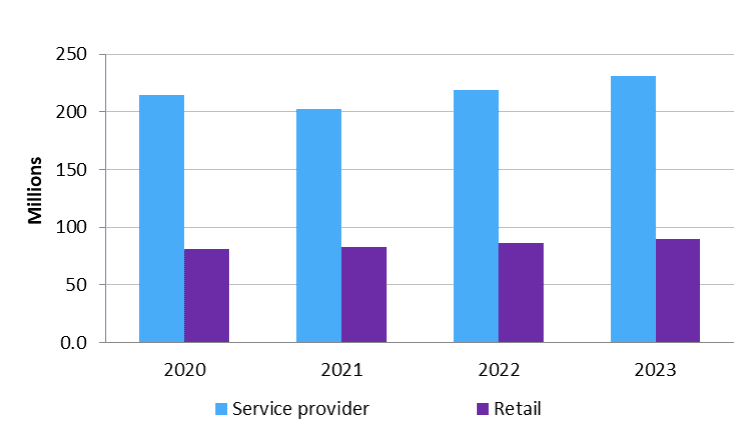

Source: Omdia

Incumbent network equipment providers (NEPs) will have similar strategies, with CPE sales tied closely to infrastructure bundles. It will, however, be important to differentiate strategies between access equipment and consumer premise equipment as interoperability becomes more important. The ability to deliver broadband is very different from the ability to propagate that throughout a household. It will be important to keep an eye on access vendors such as Huawei, Nokia, and ZTE, which will seek to keep an end-to-end solution for service providers. They will be giving solutions with advanced Wi-Fi and networking capabilities.

The likes of Sagemcom and Technicolor, who lack the infrastructure business, will need to announce more complex features for their CPE. As a result of this, average selling prices will be pushed up. They must prove this is worth the additional cost to service providers while positioned against incumbent NEPs.

Retail players such as Netgear, TP-Link, Amazon, and Google may not be as visible at MWC; however, these vendors will also be looking for partnerships with service providers to offer their CPE. They will be competing directly with the challengers to prove value to both service providers and consumers.

You can meet with Omdia's expert team at the following events:

Cable Europe (June 21, location TBC)

Carrier Billing (September 27–28, Berlin)

Broadband World Forum (October 18–20, Amsterdam)