Jonathan Doran - Principal Analyst

Some of the discussions taking place at MWC 2022 in the context of the unfolding aggregation climate will revolve around how to overcome service integration challenges (both technical and commercial).

Operators will be looking for ways to work more effectively with multiple online video partners and will be seeking effective and meaningful support from vendors to help execute their aggregation strategies. MWC being a vendor-oriented show, we expect to see further improvements in how BSS vendors facilitate smooth and flexible onboarding of online video services for CSPs, as well as continued evolution of charging systems to allow for more services and more flexibility around pricing and packaging options.

Beyond traditional multiservice bundling, streaming video represents the most widely offered and highly adopted digital value-added service in the telco consumer portfolio. In the emerging consumer-bundle landscape, streaming video will serve as both a complement and an alternative to traditional pay TV.

Source: Omdia

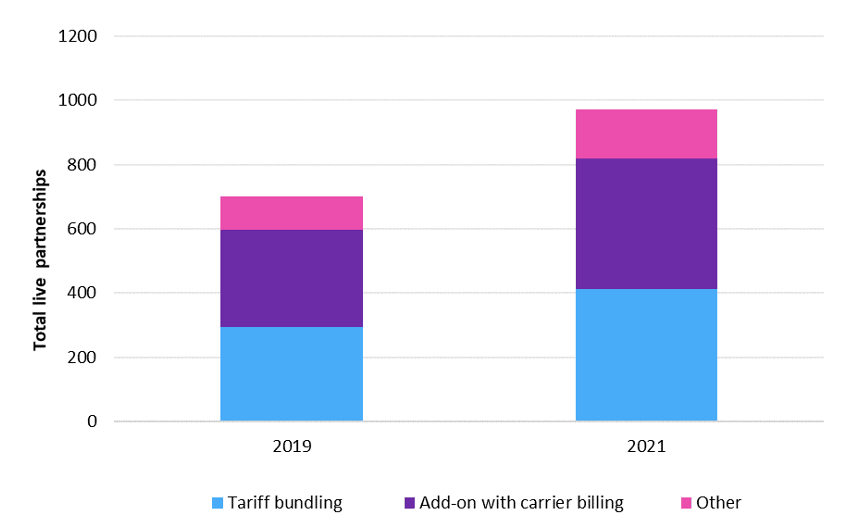

Most telcos now offer third-party streaming video either as a paid add-on or in a subsidized bundle, with a choice of multiple partner services rapidly becoming the norm. Currently, over 300 local opcos are providing bundled or carrier-billed access to third-party online video, aggregating an average of three partner services each. Meanwhile, nearly 200 service providers are hosting a growing lineup of partner streaming apps via their pay-TV or streaming video platforms, with any of these also being carrier billed and/or bundled into subscription plans.

Streaming video is the most common digital value-added service (VAS) that consumers receive within their telco offerings, with over half of paid online video users accessing these services via their fixed broadband or mobile provider. This proportion will increase further in 2022 as telcos step up their efforts to accommodate growing consumer demand for multiple streaming options.

Sitting at the heart of telcos’ billing systems, Amdocs will continue to showcase the ways in which it helps CSPs improve onboarding and monetization of OTT partner services. The content super-aggregation business model is now well established throughout the telecom industry, but integration, scalability, subscription management, and data management are still challenging service providers and partners. We expect Amdocs to show marketplace-based capability for OTT monetization.

Billing and mobile wallets provider Fortumo pairs telcos with digital merchants to facilitate payment mechanisms, with significant presence in markets where credit card penetration is limited. Expect to see demos of its turnkey bundling solution that offers analytics support and rapid time to market for CSPs entering the digital media aggregation space.

Synamedia’s well-established online video platform offering supports SPs in migrating traditional pay-TV services to a hybrid distribution environment. Among the capabilities the vendor is likely to highlight from its wide-ranging portfolio will be the seamless integration of operators’ own-brand TV offerings with those of third-party OTT providers.

You can meet with Omdia's expert team at the following events:

Cable Europe (June 21, location TBC)

Carrier Billing (September 27–28, Berlin)

Broadband World Forum (October 18–20, Amsterdam)